AKSHAYA TRITIYA GOLD MARKET GOLD PRICES GOLD JEWELLERY DIGITAL GOLD GOLD ETFS GOLD COINS GOLD BARS INVESTMENT BEHAVIOUR CONSUMER SENTIMENT PREMIUM JEWELLERY MASS MARKET LIGHTWEIGHT JEWELLERY GOLD DEMAND GOLD INVESTMENT INDIAN CONSUMERS CUL NATIONAL

MUMBAI, MAHARASHTRA, INDIA

By IFAB MEDIA - NEWS BUREAU - May 12, 2026 | 125 15 minutes read

Let’s start with what shouldn’t have happened.

This Akshaya Tritiya, gold jewellery volumes in India fell by roughly 25–30%.

And yet, the market still clocked over ₹20,000 crore in value.

Same festival. Same cultural trigger. Less gold bought. More money spent.

That is not a slowdown.

That is a structural shift.

_______________________________________________________________________________________

A few months ago, I wrote about how gold demand didn’t collapse when prices surged — it adapted.

People bought less. They shifted formats. They reduced grammage.

Demand didn’t break. It bent.

What we’ve just seen goes one step further.

Demand didn’t just bend.

It reorganised.

______________________________________________________________________________________________________________________________________________________________________________________

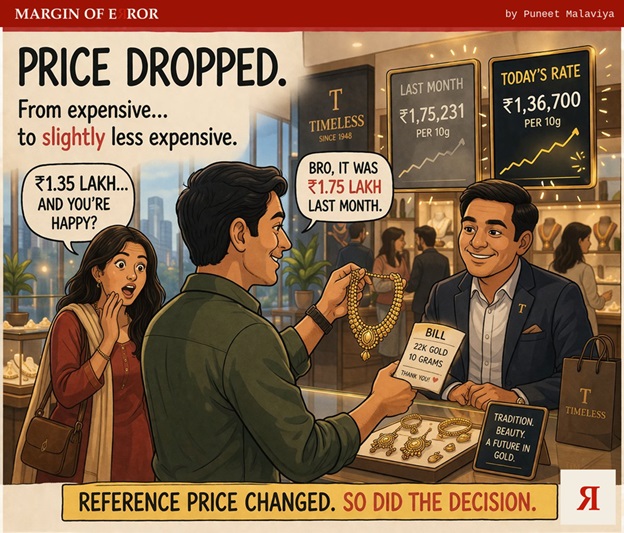

Because when prices moved from ~₹1.1 lakh to ~₹1.7 lakh in a matter of months, something fundamental changed.

Not affordability.

Expectation.

Once ₹1.7 lakh became real, ₹1.3–1.4 lakh stopped feeling expensive.

It started feeling like a window.

The price didn’t correct enough.

The reference point moved.

_______________________________________________________________________________________

And when the reference point moves, behaviour follows.

But not in one direction.

In multiple.

_______________________________________________________________________________________

Start with jewellery.

Volumes dropped sharply.

But participation didn’t.

Consumers didn’t exit the market. They resized themselves inside it.

- Lighter pieces

- Lower grammage

- Tighter budgets

Jewellery didn’t lose relevance.

It lost weight.

_______________________________________________________________________________________

Then came coins and bars.

In many markets, they outperformed traditional jewellery.

No making charges. Lower ticket sizes. Cleaner math.

This wasn’t a fallback.

It was a recalibration.

Gold was still being bought.

Just without the excess.

_______________________________________________________________________________________

At the same time, another layer accelerated quietly.

Digital gold and ETFs.

From ₹1 UPI purchases to systematic investing, participation expanded beyond the store.

Gold stopped being just something you wear.

It became something you allocate.

Convenience, liquidity and cost efficiency were no longer bundled with emotion.

They were separated.

Chosen deliberately.

_______________________________________________________________________________________

And then there’s what didn’t happen.

Old gold didn’t flood the market.

Households didn’t rush to sell into high prices.

They held.

Waiting.

Because they expect higher prices.

That is not how people behave with jewellery.

That is how they behave with assets.

_______________________________________________________________________________________

What’s becoming clearer now is that this shift isn’t uniform.

Premium demand — especially at the top end — has remained resilient.

The adjustment is happening lower down the ladder.

Which means the same price shock didn’t create one market response.

It created two.

The same price created two different markets.

_______________________________________________________________________________________

At the same time, parts of gold started behaving differently altogether.

At the premium end, higher prices didn’t suppress demand.

They reinforced it.

Expensive gold didn’t become harder to justify.

It became more meaningful to own.

Not despite the price.

But because of it.

_______________________________________________________________________________________

And the proof is no longer just behavioural.

It’s visible in the market.

Jewellery companies operating in the same category, under the same gold price environment, are delivering completely different outcomes.

Some have seen strong growth.

Others have declined.

Same gold. Different results.

Demand didn’t disappear.

It stopped behaving uniformly.

______________________________________________________________________________________

Now bring it back to the moment that triggered all of this.

Akshaya Tritiya.

A day when buying gold is not just a transaction.

It is participation.

People don’t ask:

“Is this the right price to buy?”

They ask:

“How much should I buy?”

And that shift in question explains everything.

_______________________________________________________________________________________

So what does the Indian gold market look like today?

The same consumer is now doing three different things:

Buying less jewellery per transaction — but continuing to show up.

Allocating more to coins, ETFs and digital gold — behaving like an investor.

Holding on to existing gold — behaving like someone expecting future gains.

Three behaviours. Three logics. One category.

_______________________________________________________________________________________

Which leads to the real shift.

Gold is no longer one thing.

It has split into:

- Jewellery (expression)

- Investment (allocation)

- Culture (participation)

And now, even within jewellery:

- Premium vs mass

- Heavy vs light

- Design vs weight

- _______________________________________________________________________________________

This is not a demand story.

This is a structure story.

_______________________________________________________________________________________

The price didn’t break India’s relationship with gold.

It broke the way that relationship was expressed.

_______________________________________________________________________________________

And that’s why this Akshaya Tritiya matters.

Because it proves something most people are still missing.

People didn’t stop buying gold.

They just changed how they showed up.

_______________________________________________________________________________________

If you think this is about gold prices, you’re still looking at the surface.

This is about what happens when a category becomes expensive faster than consumers can process.

They don’t walk away.

They adapt. They fragment.

They rationalise.

_______________________________________________________________________________________

And sometimes…

They don’t change at all.

_______________________________________________________________________________________

The format changed.

The compulsion didn’t.

|

Puneet Malaviya - Lead Marketing, Raymond Lifestyle Ltd

Puneet Malaviya is a distinguished marketing leader with nearly two decades of impactful experience in driving brand growth, customer engagement, and retail excellence across India’s consumer landscape. Currently a brand marketing lead for Raymond handling multiple brands like Ethnix by Raymond, Raymond Home & New Businesses Vertical at Raymond Lifestyle Ltd , Puneet is known for his strategic vision and ability to create meaningful brand experiences in the competitive fashion and lifestyle sector.

Over his accomplished career, Puneet has held senior leadership roles at prominent brands including Head of Marketing at TBZ – The Original and DGM – Marketing at Spencer’s Retail, where he played key roles in expanding market presence and strengthening brand value. His professional journey spans diverse domains such as customer relationship management, retail strategy, and omni-channel marketing, demonstrating both depth and breadth of expertise.

Puneet’s leadership has been instrumental in spearheading innovative campaigns and initiatives that resonate with consumers and deliver measurable results. His efforts contribute not only to business growth but also to enhancing brand relevance in a rapidly evolving market.

He holds a Post Graduate Diploma in Business Management (Marketing) from Chetana’s Institute of Management and a Bachelor of Science from the University of Allahabad, grounding his professional accomplishments in strong academic foundations. |

Follow Margin of Error on Substack : https://marginoferrorhq.substack.com/ Margin of Error Retail decision science. Where data ends and judgment begins.